Company Update / Plantation / IJ / Click here for full PDF version

Author(s): RyanDimitry

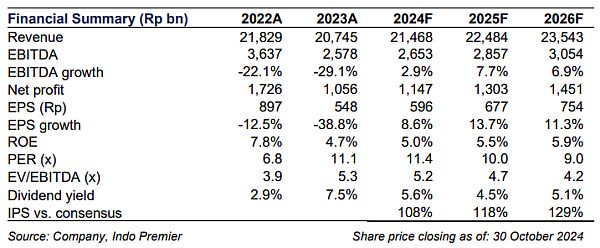

- 9M24 net profit of Rp801bn (flat yoy) was in-line with our consensus but above our expectation due to higher-than-expected top line growth.

- However, 3Q24 net profit was weaker at Rp300bn (-31% yoy/+11% qoq) as sales/production volume was weaker due to ageing plantation profile.

- We maintain our Hold call with a higher TP of Rp7,300 as continued to face production issues despite the higher CPO prices.

9M24 net profit came in-line with consensus but above our estimates

9M24 net profit reached Rp801bn (flat yoy) in-line with consensus at 73% but above ours at 76% (vs. a 3Y avg of 74%), due to higher-than-expected top-line growth from higher CPO ASP. Revenue reached Rp16.3tr (+4% yoy) as growth in CPO ASP (+3% yoy) was able to offset a decline in sales volume (-2% yoy). Gross profit grew to Rp2tr (+4% yoy) as GPM was flat at 12% (-12bps yoy). EBIT grew to Rp947bn (+9% yoy) as EBIT margin was stable at 6% (+30bps yoy) driven by logistics cost efficiencies in selling expenses (-16% yoy).

3Q24 net profit declined due to weak top-line growth

Net profit declined to Rp300bn (-31% yoy/+11% qoq) due to weak top-line growth. Revenue reached Rp6.0tr (-5% yoy/+8% qoq) as sales volume declined (-19% yoy) due to lower production on ageing plantation profile. Its gross profit reached Rp722bn (-22% yoy/+3% qoq) as GPM declined to 12% (-257 bps yoy/-64 bps qoq) from lower operating leverage. Its EBIT reached Rp367bn (-31% yoy/+8% qoq) while EBIT margin also declined to 6% (-234 bps yoy/-64 bps qoq).

CPO production declined along with sales volume despite ASP increase

Operationally, we saw a decrease in CPO production at -20% yoy/flat qoq to 287kt in 3Q24, FFB production also declined by -23% yoy/-3% qoq to 925kt. FFB yield also declined to 14t/ha in 3Q24 from 18t/ha in 3Q23. In terms of sales volume, CPO sales also declined -19% yoy/-2% qoq to 284kt in 3Q24 despite rising CPO ASP to Rp12.2k/t in 3Q24 (Rp11.6k/t in 9M24) which was up 13% yoy/+10% qoq.

Maintain Hold with a higher TP of Rp7,300

We adjusted our FY24-26F EPS by 1-2% to incorporate 3Q24 data points, due to higher CPO ASP and lower GPM. Resulting in a higher TP of Rp7,300/sh (vs. Rp7,200 previously). However, we maintain our hold rating on amid risk to production volume on issues of aging plantation profile. is currently trading at 11.4x FY24F P/E. Upside risk is higher CPO prices for FY25F.

Sumber : IPS